To most, living in the moment is easy. You spend on whatever pleases you. But is there a limit to it? Knowing that retirement will come one day, you have to save money for the future because you can’t work forever. Old age and illness will kick in. If you want to enjoy life in your golden years like how you’re enjoying it now (or even better!), you need to be deliberate in planning for your retirement. Here are five tips to help you achieve your retirement goals:

1. Visualise what your desired retirement lifestyle looks like

It starts with knowing what you want.

When do you want to retire? Do you want to retire early, or do you want to hold off as long as possible because you enjoy your work? What kind of lifestyle do you want to have during your retirement years? Minimal, comfort, or luxury?

What types of expenses are you expecting? Basic needs or comfort items, such as travelling abroad?

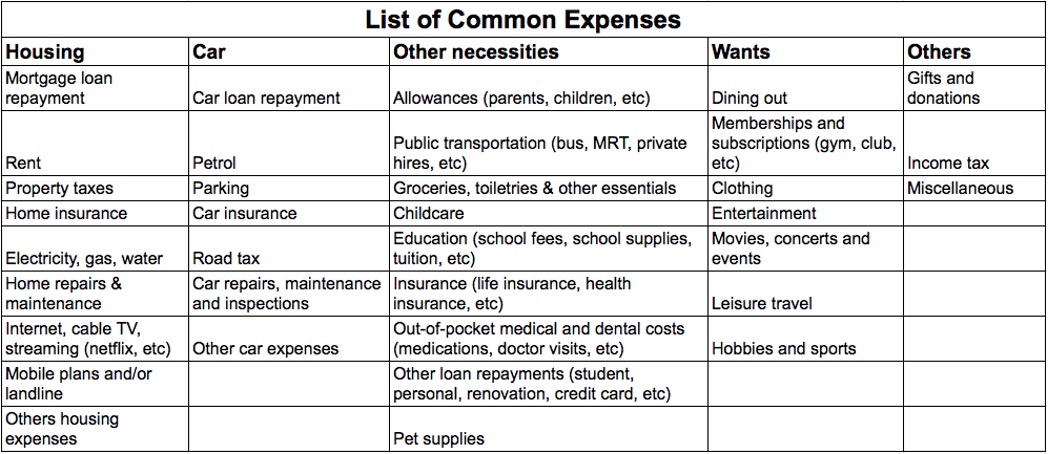

Here are some common expenses:

Doing this activity allows you to paint a picture of what you want. This is critical as retirement is often so far away that we can’t see it, and as such, we tend to lose sight of what we’re saving for.

2. Find out how much you need during retirement

By now, you should know what kinds of expenses to expect during retirement. While there are many ways to calculate how much you need to save, here’s a simple way.

The first step is to put an amount to each cost item in today’s value, and tabulate the total monthly cost. Because this figure is in today’s value, you’ll have to estimate how much it’ll cost in the future to account for inflation. You can assume an average inflation rate of 3%. This inflated monthly figure will then be able to sustain your desired lifestyle.

But how long do you need this monthly amount? You can use the average life expectancy (which is currently at 83.6 years) as a reference. In short, to calculate how much retirement money you’ll need at retirement age, you can use this formula:

Total Retirement Fund Needed = Inflated Monthly Expenses * (Average Life Expectancy – Retirement Age)

That’ll give you a rough estimate of how much you need during retirement.

3. Consolidate your current finances

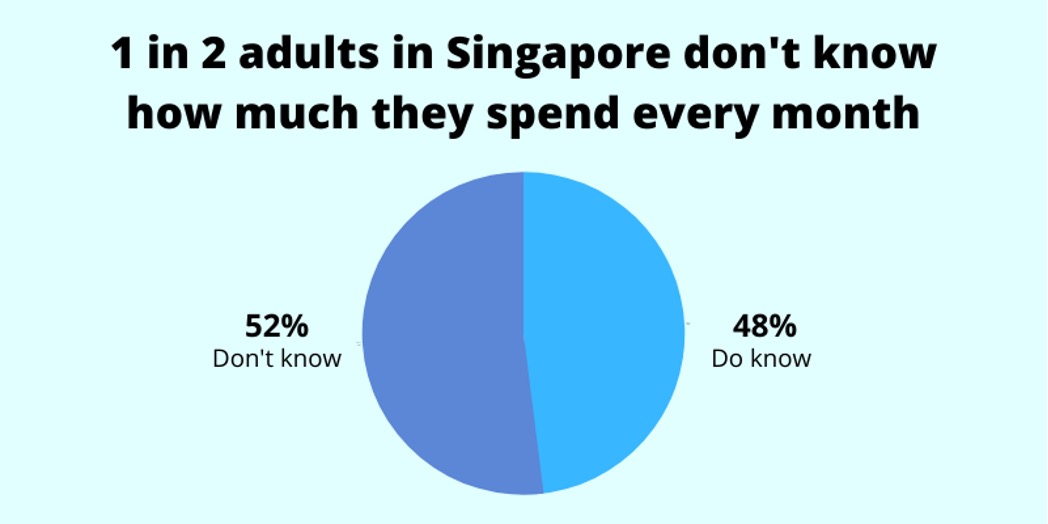

Do Singaporeans know their finances well? When we look at some spending habits of Singaporeans, that doesn’t seem to be the case. One in two adults in Singapore doesn’t even know how much they spend every month. So if you’ve not been regularly reviewing your assets, liabilities, income, and expenses, it’s time to start.

Although it can be seen as cumbersome, once you’ve done it, you’ll know where you stand and what can be improved upon.

If you haven’t done this before, it might take some effort on your part, so try to take smaller steps. If not, you may give up easily.

4. Calculate your shortfall

Simply take the retirement fund needed and subtract it from the assets you have right now (meant for retirement). This will then be your retirement shortfall.

If you don’t have a shortfall, that’s good news. Continue to do what you’re doing and you’ll have no problems retiring. If there’s a shortfall, know that something has to be done.

If you continue to save at your current rate, are you able to eliminate this shortfall? If not, you might need to have a higher savings rate. And if you’re not able to achieve your goal even with a higher savings rate, then, even more, should be done.

5. Look for solutions to grow your money

Outside of emergency funds and money set aside for short-term financial goals, your excess cash in the bank should be put into better use.

This is especially so when your retirement shortfall is too big and simply saving will not be enough. Therefore, the solution to that problem is to find ways to either increase your income or to invest your money.

There are many investment alternatives out there, but you should always pay attention to your time horizon, risk preferences, and expected returns.