Even at my not so tender age of early 30s, I am surprised that many of my peers are still not making plans for retirement. But at least they do have some savings, unlike our Gen Y Singaporeans who swear by the ‘Live The Moment’ mentality. Some of them are literally hanging by the thread waiting for their next pay check. It is hence little wonder why our government is panicking, increasing our CPF minimal sum, lengthening our retirement age etc. Gosh, with ever increasing cost of living and eroding importance on savings – Has retirement in Singapore become an urban legend?

Need To Plan So Early Meh?

Having crossed the big 30, we are already halfway through the race. We should be evaluating our spending habits and make appropriate adjustments for regular retirement savings. Starting early has its advantages, you will have a longer time horizon and that means more time to grow your savings and ride out short term fluctuations on your investments if any.

If you are already in your 40s and yet to start planning, you will have to work harder at growing your retirement savings. That is provided that you keep your job, many Singaporeans Professional, Managers & Executives (PMEs) find it hard to retain employment or get re-employed past the age of 40. Worst case scenario, you may even need to think of delaying your retirement age.

How Much Is Enough?

That my friend is a tricky question. It will depends on your preferred retirement age, projected lifespan and how comfortable you want your retirement to be.

Singaporeans are living longer and healthier with average life expectancy for males and females higher than before. Hence when you are planning for your retirement, do take note of the number of years you would expect your savings to last you, as you would want to avoid a situation where you outlive your retirement funds.

Do a quick mental calculation to find out the amount of money you will need when you retire to provide for your desired lifestyle. Financial planners would generally recommend at least two thirds of your last drawn monthly income.

Here’s a rough calculation to get you thinking. Assuming that Mr Average PME plan to retire at the age of 60 and he projects that he will live till a ripe old age of 85 years old. His last drawn salary is S$5,000. This mean that he will need to draw down around $3,500 from his retirement funds each month to provide for his desired lifestyle.

Throwing interest and inflation from 60 years to 85 years old out of the window, the rough amount that he needs for retirement:

(85 – 60) years x 12 months x S$3,500 = $1,005,000

This amount by the way should be accessible cash, the value of the property that he is living in should not be placed within the equation. You may think that at retirement, you can spend lower than $3,500. Think again – if you are used to dining at restaurants, are you sure you can give it up totally for kopitiam everyday? What happens when your friends invite you for meals? Will you decline because you did not cater enough for your retirement?

What if you face large bills such as your children’s university fees or medical bills (Medisave cannot be used to pay all types of medical bills and there is a limit to how much Medisave you can use for approved procedures)? Do you need to continue to purchase private health insurance even after Medishield Life kicks in?

In addition, S$1,005,000 is before taking inflation into account. If you put your money in a bank savings account where the pathetic interest rates are much lower than inflation, this amount will not be able to sustain your current lifestyle.

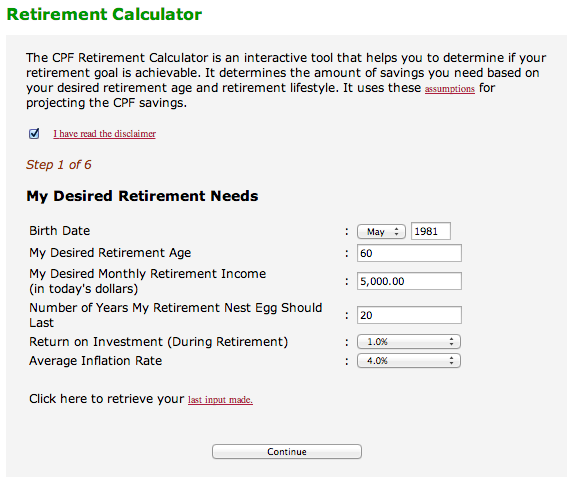

The above example is just a rough calculation. There are many online tools that can help you with the computations. The CPF retirement estimator gives you a quick overview of how much you need to set aside for your retirement.

Time To Press The Panic Button

Do you want to panic only when you’re retired? However you do not need to freak out now as you still have time on your side.

Calm down and work out your current financial status. This means adding up all the money in your savings account, CPF savings, insurance policies, and investments and do a projection of their future value at the time when you retire. You should also aim to pay off any outstanding loans and liabilities before retirement to minimise debt obligations during your golden years.

Review your insurance coverage. Healthcare costs will rise very quickly as you get older and could derail your financial plans. If you do not have any insurance coverage, you may wish to consider purchasing coverage for possibilities such as disability, critical illnesses, personal accident and hospitalisation.

If you have purchased health insurance coverage, you should ensure that your retirement years are covered, and/or explore possible options where you can stop paying premiums once you reach retirement age but still continue to enjoy the coverage. You will be glad to know that our government has just enhanced and made it compulsory for all Singaporeans and PR to upgrade to CPF MediShield Life where even those with preexisting illnesses are covered.

Calculate the difference between the funds you expect to have at retirement and the amount you will need. Then work backwards to find out how much you need to start saving each month from today in order to make up for this shortfall.

Cut back on luxury products and services and make a conscious effort to slash away larger portion of your monthly income for retirement. Depending on your risk appetite, you can examine existing financial products and built a well-diversified portfolio that will help to spread the risk and balance the fluctuations in your investment.

Get Started On Your Retirement Savings

Yes, you have to quickly put in place a retirement plan to help you save or invest regularly to accumulate your retirement savings.

Cut back on luxury products and services and make a conscious effort to slash away larger portion of your monthly income for retirement. Depending on your risk appetite, you can examine existing financial products and built a well-diversified portfolio that will help to spread the risk and balance the fluctuations in your investment.

I Cannot Do It On My Own!

If you are starting out late or feel that you are unable to save enough for retirement due to your existing income or other commitments, fret not! Our efficient government have the following in place to help you get closer to your retirement goals.

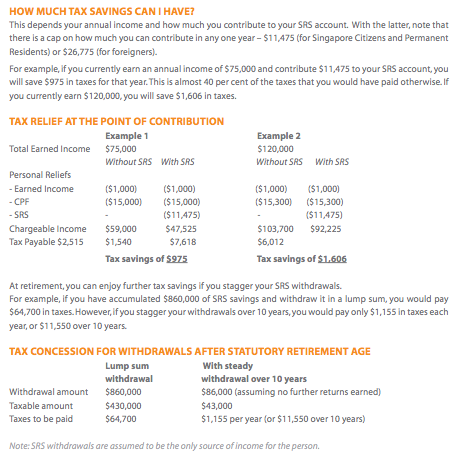

1. Supplementary Retirement Scheme (SRS)

The government has put in place the Supplementary Retirement Scheme (SRS) which provides tax benefits to encourage saving for your retirement.

2. Delaying Re-employment Age Limit From 65 To 67

Companies in Singapore are now obliged to offer re-employment to workers who turn 62, up to 65. But NTUC Deputy Chief Heng Chee How hopes to push the re-employment age ceiling to 67 so this would give older workers who wish to continue working a chance to do so, and longer employment helps to extend the CPF contribution period to help increase CPF savings and hence retirement adequacy.

This means if you haven’t saved up enough, you have a longer employable lifespan to close the gap.

3. Increasing CPF Contribution Through Progressive Wage Model

NTUC has been actively pushing for sustainable wage increases for all workers through a raise in productivity, skills and career paths, aka Progressive Wage Model.

This idea is one that has been repeated over and over again by Mr Lim Swee Say who believes that workers deserve wages more than the minimum wage if they become better workers based on their skills, productivity and perform value added duties.

NTUC has been providing Inclusive Growth Programme funding and know-how to support companies who are willing to innovate, adopt the use of new technology and make structural changes to enhance their productivity. With higher wages, all workers can enjoy increased contribution to CPF.

Look for companies that offer you a form of Progressive Wage Model such as clearly outlined career ladders, training assistance and learning opportunities to improve your productivity.

4. Pledge Your Property

Singaporeans also have the option of pledging their properties to reduce the CPF minimum sum by half.

Assuming the value of the property is worth more than the pledge amount, which is half of the current CPF minimum sum, then the minimum sum required is only $77,500 (from $155,000). The reason for this is that if you own a home and live in it, you do not have to pay rental, which decreases your monthly expenses dramatically.

Check out other ways which you can reduce your CPF minimum sum, but take note that it also means you should already have alternate sources of passive income which fulfil the purpose of retirement adequacy that the CPF minimum sum was set up for.

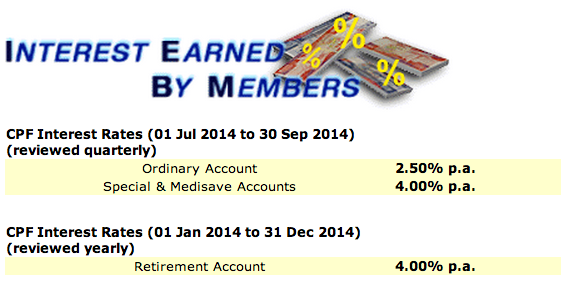

If you are unfamiliar with investing in high risk financial instruments, depending on CPF as one source (not the only source) for future retirement funds may not be a bad idea as you are guaranteed the interest rates below but bear no investment risk to your CPF assets.

Retirement Planning Is Not An Urban Myth

With the coming of the silver tsunami, retirement adequacy is an area that all Singaporeans should pay attention to. Our government has to ensure that our ageing population is able to look after ourselves well and not be an unbearable strain on the significantly smaller working population.

Schemes and plans have been put in place by NTUC and government to give all Singaporeans a fighting chance to enjoy their golden years. They can only do so much; the rest is up to us.